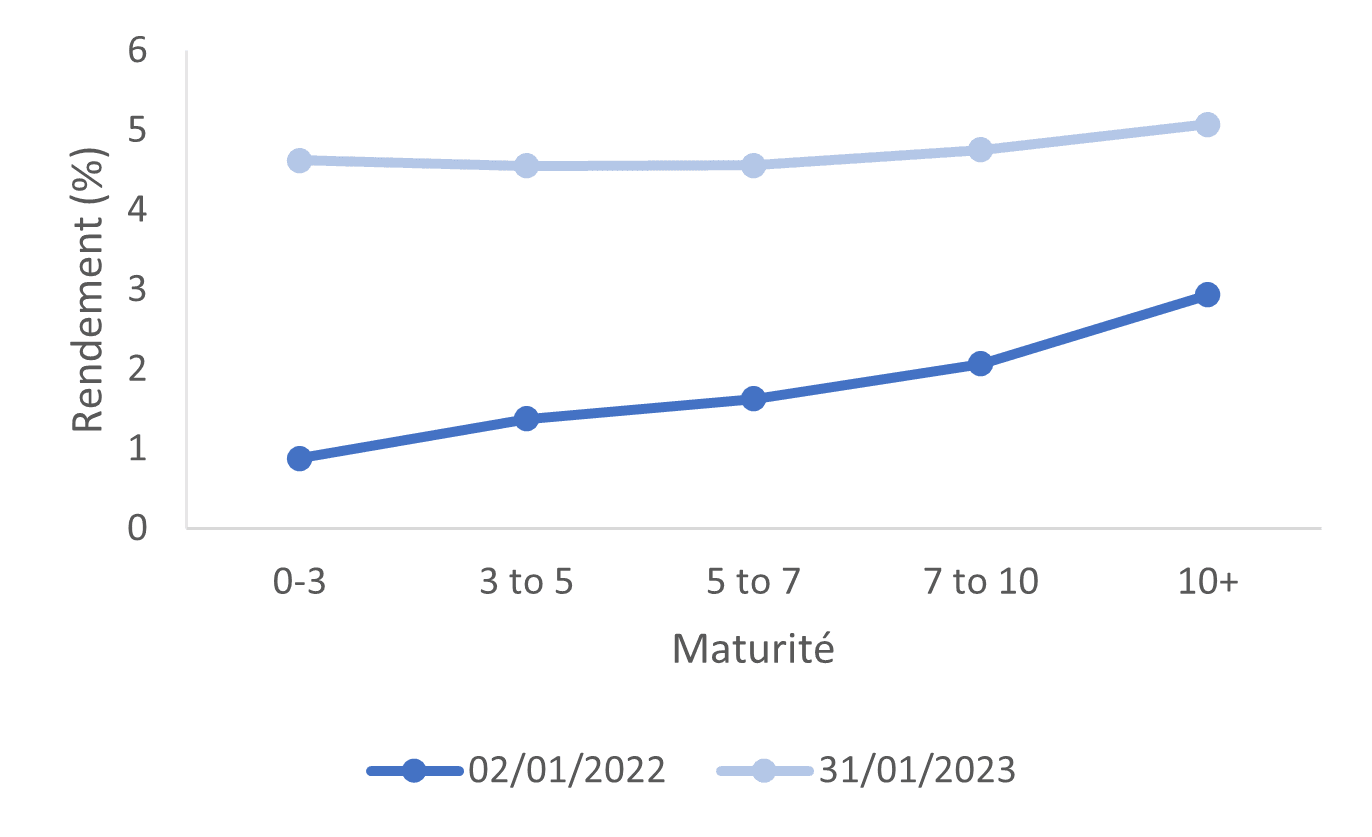

1. Increase exposure to longer duration assets

2022 has been a difficult year for all credit markets, given the inflationary pressures and resulting interest rate hikes. Assets with longer duration were sold off in particular. However, rates markets have rallied over the past three months and the forward rate curve is no longer trending up as future rate movements are priced in; we might see the end of central bank rate hikes by the middle of the year.

Given the improving rate environment, we believe there are growing short-term opportunities in longer duration (around 8-10 years) and higher quality (investment grade rated) credits. which tend to exhibit lower volatility and maintain their relationship to returns. We believe that this sub-section of corporate credit is likely to rebound in correlation with the fall in rates.

Graph. 1 – The market indicates that the Fed is near the end of the rate hike cycle.

- Source: Bloomberg as of January 23, 2023. For illustrative purposes only, not to be construed as investment advice

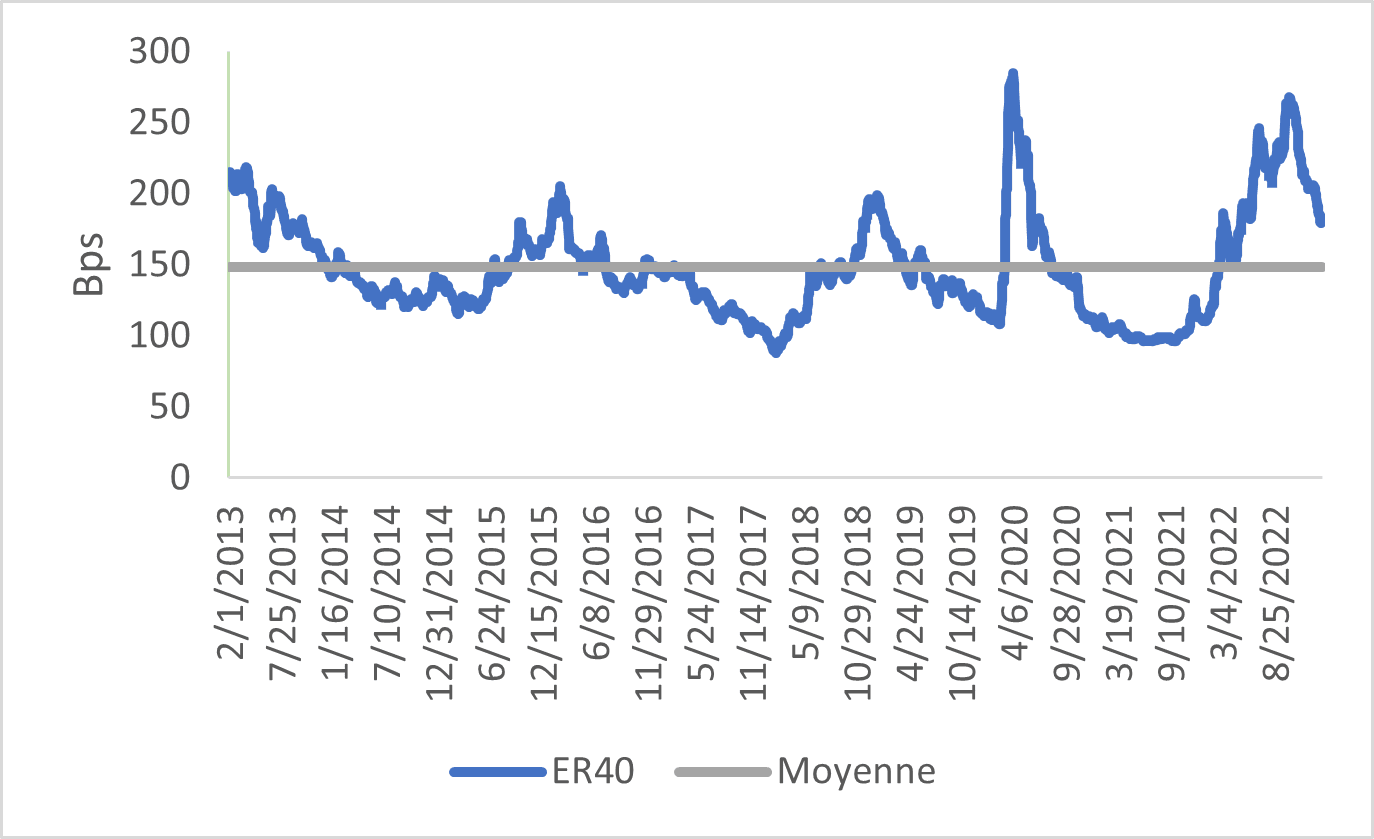

2. Opportunities in short duration high yield securities

Given the large swings in yields on the front end of the curve, we also see opportunities in higher yielding, short duration assets. Bonds of the BBB and BB categories have a very attractive yield per unit of duration. Due to the relatively flat yield curves, investors are compensated for taking the same level of risk in both short and long duration assets.

Graph. 2 – Short-duration investment grade yields look attractive

- Source: ICE Data Platform, as of January 31, 2022. ICE BofA Global Corporate Index (G0BC). For illustrative purposes only, not to be construed as investment advice.

3. European credit

European and euro-denominated assets were hit hard by Russia’s invasion of Ukraine last year. However, we now see value in Euro assets and have increased our exposure in the shorter duration BBB segment. We also see value in European financials, both for senior bonds and subordinated debt (lower tier 2) because European banks are in good financial health in our view; they are backed by the European Central Bank and their securities have been significantly revalued, particularly in the subordinated segment where yields are very attractive.

Graph. 3 – European BBBs are approaching the 10-year average

- Source: ICE Data Platform, as of January 31, 2022. ICE BofA Global Corporate Index (G0BC). For illustrative purposes only, not to be construed as investment advice.

Conclusion

Multi-asset credit strategies can navigate between different credit asset subclasses, ratings and regions to find the most attractive valuations while reducing risk exposure during times of heightened volatility. Although valuations have tightened considerably in recent months, we remain constructive on credit.