2023-04-25 19:10:11

People walk by the New York Stock Exchange (NYSE) on February 14, 2023 in New York City.

Spencer Platt | Getty Images

A banking crisis that erupted less than two months ago now appears to be less a major broadside to the U.S. economy than a slow bleed that will seep its way through and act as a potential catalyst for a much-anticipated recession later this year.

As banks report the impact that a run on deposits has had on their operations, the picture is a mixed one: Larger institutions like JPMorgan Chase and Bank of America sustained far less of a hit, while smaller counterparts such as First Republic face a much tougher slog and a fight for survival.

That means the money pipeline to Wall Street remains mostly alive and well while the situation on Main Street is much more in flux.

“The small banks are going to be lending less. That’s a credit hit on Middle America, on Main Street,” said Steven Blitz, chief U.S. economist at TS Lombard. “That’s negative for growth.”

How negative will come to light both in the approaching days and months months as data flows through.

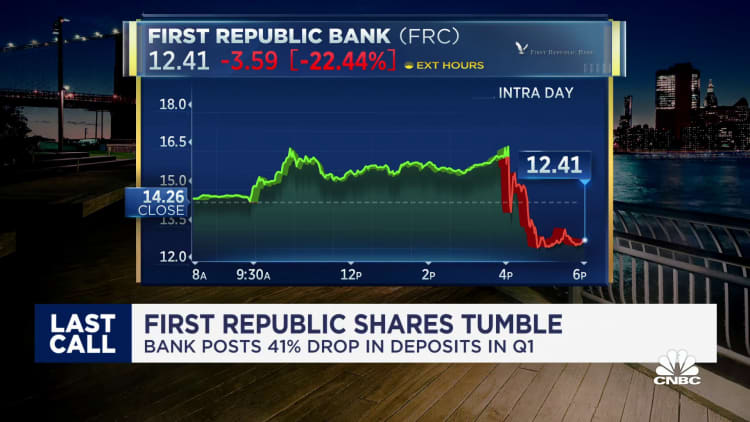

First Republic, a regional lender seen as a bellwether for how hard the deposit crunch will hit the sector, posted earnings that beat expectations but reflected a struggling company otherwise.

Bank earnings largely have been decent for the first quarter, but the sector’s future is uncertain. Stocks have been under pressure, with the SPDR S&P Bank ETF (KBE) off more than 3% in Tuesday followingnoon trading.

“Rather than bringing concerning new information, this week’s earnings are confirming that the banking stress stabilized by the end of March and was contained at a limit set of banks,” Citigroup global economist Robert Sockin said in a client note. “That’s regarding the best macro outcome that might have been hoped for when stresses emerged last month.”

Watching growth ahead

In the immediate future, the reading on first-quarter economic growth is expected to be largely positive despite the banking problems.

When the Commerce Department releases its initial estimate on gross domestic product gains for the first three months of the year, it’s expected to show an increase of 2%, according to the Dow Jones estimate. The Atlanta Fed’s data tracker is projecting an even better gain of 2.5%.

That growth, though, isn’t expected to last, due primarily to two interconnected factors: the Federal Reserve interest rate hikes aimed purposely at cooling the economy and bringing down inflation, and the constraints on small-bank lending. First Republic, for one, reported that it suffered a more than 40% decline in deposits, part of a $563 billion drawdown this year among U.S. banks that will make it tougher to lend.

Yet Blitz and many of his colleagues still expect any recession to be shallow and short-lived.

“Everything keeps telling me that. Can you have a recession that is not led by autos and housing? Yes, you can. It’s a recession created by a loss of assets, a loss of income and that eventually flows through to everything,” he said. “Again, it’s a mild recession. A 2008-2009 recession occurs every 40 years. It’s not a 10-year event.”

In fact, the most recent recession was just two years ago in the early days of the Covid crisis. The downturn was historically steep and short, ended by an equally unprecedented fusillade of fiscal and monetary stimulus that continues to flow through the economy.

Consumer spending has seemed to hold up fairly well in the face of the banking crisis, with Citigroup estimating excess savings of regarding $1 trillion still available. However, delinquency rates and balances are both rising: Moody’s reported Tuesday that credit card charge-offs were 2.6% in the first quarter, rising by 0.57% from the fourth quarter of 2022, while balances soared 20.1% on an annual basis.

Personal savings rates also have tumbled, falling from 13.4% in 2021 to 4.6% in February.

But the most comprehensive report released so far that takes into account the period when Silicon Valley Bank and Signature Bank were shuttered indicated that the damage has been confined. The Federal Reserve’s periodic “Beige Book” report released, April 19, indicated only that lending and demand for loans “generally declined” and standards tightened “amid increased uncertainty and concerns regarding liquidity.”

“The fallout from the crisis seems less serious than I had expected just a few weeks ago,” said Mark Zandi, chief economist at Moody’s Analytics. The Fed report “was a lot less hair-on-fire than I had expected. [The banking situation] is a headwind, but it’s not a gale-force headwind, it’s just kind of a nuisance.”

It’s all regarding the consumer

Where things go from here depends greatly on the consumers who account for more than two-thirds of all U.S. economic activity.

While the demand for services is catching up to pre-pandemic levels, cracks are forming. Along with the rise in credit card balances and delinquencies is likely to come the further obstacle of tightening credit standards, both by necessity and through an increased likelihood of tougher regulation.

Lower-income consumers have been facing pressure for years as the share of wealth held by the top 1% of earners has continued to climb, up from 29.7% when Covid hit to 31.9% as of mid-2022, according to the most recent Fed data available.

“Before any of this really started unfolding in early March, you were already starting to see signs of contraction and reining in of credit,” said Jim Baird, chief investment officer at Plante Moran Financial Advisors. “You’re seeing reduced demand for credit as consumers and businesses start to pull in the deck chairs.”

Baird, though, also sees chances slim for a steep recession.

“When you look at how all the forward-looking data lines up, it’s hard to envision how we sidestep at least a minor recession,” he said. “The real question is how far can the strength of the labor economy and still-significant cash reserves that many households have propel consumers forward and keep the economy on track.”

1682509112

#banking #crisis #slowburn #impact #economy