As IDC had anticipated over the summer, spending on cloud computing and storage infrastructure continued to grow strongly in the third quarter, helped in particular by large backlogs and improved supply chains. They thus increased by 24.7% year-on-year to reach $23.9 billion. The non-cloud segment is also doing quite well with a 16.5% increase in spending to $16.8 billion.

Spending on cloud infrastructure is divided into $16.8 billion for shared infrastructure (+24.4%) and $7.1 billion for dedicated infrastructure (+25.3%). For the latter, 45.2% were deployed on customer premises.

IDC forecasts the cloud infrastructure market to reach $88.1 billion by the end of 2022, a year-over-year increase of 19.6%. A performance well above that of 2021 when growth was 8.6%. Spending on shared cloud infrastructure is expected at $60.9 billion (+19%) and dedicated at $27.3 billion (+21.5%).

For their own needs, service providers (cloud, digital, communication or managed services) spent $23.9 billion in the third quarter (+22.5%) and should sign $87.8 billion in orders on the year (+17.5%).

All regions benefit from this growth in cloud infrastructure spending, with the exception of Central and Eastern Europe, whose spending plunged 35.1% in Q3 with the war in Ukraine. The Middle East and Africa region grew the most (+65.8%) ahead of the United States (+32.1%) and Western Europe (+31.3%). and 20%.

Over the year as a whole, Central and Eastern Europe should also be down. The 4 regions Asia/Pacific (excluding Japan and China), Middle East/Africa, United States and Western Europe should post growth of between 20% and 35%.

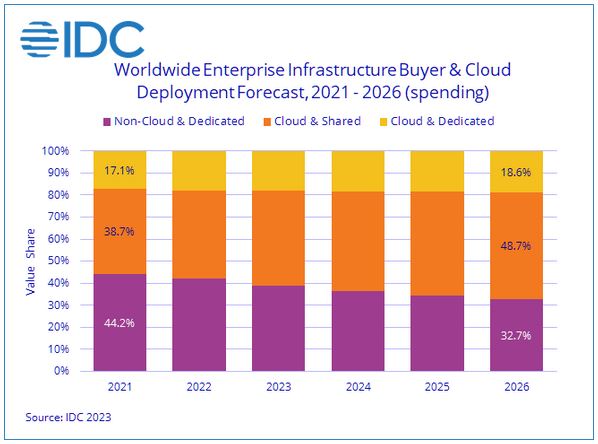

Over the period 2021-2026, IDC estimates the compound annual growth rate (CAGR) of cloud infrastructure spending at 12.9%. They should thus climb to $135.1 billion in 2026. An estimate significantly revised downwards since last July IDC was still counting on a CAGR of 14.5% and $145.2 billion in expenditure in 2026.