Although the number of new non-agricultural jobs announced on Friday (7th) in the United States was less than half of market expectations, experts said that from data such as wage increases and unemployment rates, bond market traders can almost safely assume that the Fed (Fed) There are few obstacles to raising interest rates in March, and it can even be inferred that the Fed has fallen behind. Investors should prepare for more aggressive monetary tightening. How to reduce the balance sheet (shrinking balance sheet) will be the focus.

Several key figures in the December non-agricultural employment report include:

- 199,000 people were added, which was far behind the market’s estimate of 400,000 people

- The unemployment rate dropped to 3.9%, which was better than market expectations and only dropped to 4.1%

- Wage growth has expanded, with an average hourly wage increase of 4.7% annually and 0.6% monthly, easily beating the median forecast

Therefore, even if the overall number of new additions is inferior, it still does not change the possibility of the Fed’s interest rate hike in March.U.S. stocks fell once more on Friday and U.S. Treasury yields continued to rise. The 10-year yield climbed to 1.801%, a two-year high. It has risen by 25 basis points this week, the largest week since September 2019. Increase.

The current Fed Funds rate market futures show that the probability of raising interest rates by 25 basis points (1 yard) in March is regarding 84%, and it was close to 90% in Friday’s intraday trading.

Bloomberg columnist Brian Chappatta said that although the number of new jobs is poor, it mainly reflects harsh seasonal adjustments, and the unemployment rate is heading towards the 3.5% that Fed officials believe will only reach the end of 2024.

For traders who are struggling to scrutinize the Fed’s tightening path, the December non-agricultural report is the first heavyweight economic data this year.The next highlight will be the Consumer Price Index (CPI) in December. The current market forecasts that the annual growth rate of CPI will rise to 7.1% and the annual growth rate of core CPI will rise to 5.4%, which means that both may surpass the 40-year high reached in November.. Although the Federal Open Market Committee (FOMC) routine decision-making meeting appeared at the end of January, the routine meeting on March 16 is more important.

Chappatta said that with the unemployment rate dropping to 3.9% and the inflation rate likely to remain above the central bank’s target, it is not difficult to expect the Fed to mention the words “maybe there are suitable reasons” for raising interest rates in its January statement. The Fed used the same wording before raising interest rates in 2019 and reducing bond purchases in 2021, showing that there is almost no suspense regarding raising interest rates in March.

Shrinking tables will be faster and more fierce

According to Barron’s analysis, the 3.9% unemployment rate is already lower than the Fed’s so-called natural unemployment rate (that is, the lowest unemployment rate under stable inflation).

Michael Darda, chief economist of MKM Partners, said that during the last economic expansion, when the unemployment rate fell below 4%, the Fed had entered a cycle of interest rate hikes for two years and had started to shrink its balance sheet for nearly a year. Compared with the last wave of economic expansion, the Fed is now behind the situation.”

According to Darda’s model, the neutral interest rate continues to rise. If the policy interest rate continues to remain close to zero and the neutral interest rate continues to rise, the Fed’s default policy stance will be more accommodative. A rise in neutral interest rates means that the so-called velocity of money may be regarding to rise. When the currency turnover speeds up, the economy may not be able to cope with the rising demand, which will cause the originally hot inflation to rise further.

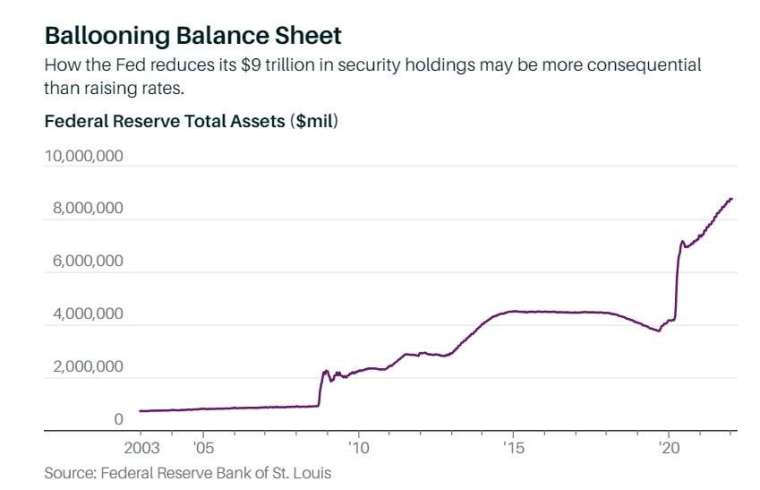

The current Fed balance sheet is close to 9 trillionDollar, The scale is twice that of the scale reduction since 2017. Fed officials said in the minutes of the December meeting released this week that they may need to shrink the balance sheet more quickly and aggressively.

Citi economist Veronica Clark predicts that the Fed may begin to shrink its balance sheet from July, and the scale of reinvestment of maturing bonds will initially be reduced by 25 billion per month.Dollar, Later changed to a monthly reduction of 75 billionDollar。

Investors should cheer for the reduction of the balance sheet

Barry Knapp, director of the Ironsides Macroeconomics research department, said that when the Fed starts to shrink its balance sheet, the real monetary tightening is true. He explained that at present, one-third of the public debt and mortgage securities market is in the hands of the Fed. Only when the Fed starts to reduce its scale can the long-term interest rate rise.

Shrinking the balance sheet would cause the stock market to collapse at first glance, but Knapp said that in fact, because monetary policy is so loose that it hinders economic growth, shrinking the balance sheet is a good thing. Taking the housing market as an example, the first buyers who really need it have been blocked from the market.

He said that the Fed’s Quantitative Easing (QE) exit will be a difficult test for the stock market in the first half of the year, but it will be an excellent benefit to the economy. He predicted that the major indexes will fall by 10% to 12% in the first half of the year due to currency tightening, and at the same time, an excellent buying point for investors to enter the market will emerge.