Everyone who is of a certain age, even a certain age (like me) remembers with terror the problems with baths and taps, with an idiot who had left the drain open while the taps were running… and it was necessary to calculate when the bathtub was going to overflow given the flows coming from the taps and the losses coming from the drain.. I still have cold sweats.

Well, I think the same problem is going to present itself to global bond markets.

Let me explain.

Let’s go back to the end of the previous century.

A terrible financial crisis is ravaging Asia.

Thailand, South Korea, Indonesia, Malaysia see their exchange rates more or less fixed on the dollar “jump” and the IMF is called to the rescue.

This financial institution does what it was created to do, that is to protect the big international banks once morest their own mistakes by impoverishing those who had the bad idea to borrow dollars from these banks, and the levels of life in Asia are collapsing.

Note in passing that this practice allows American creditors to buy assets in these countries at unbeatable prices, with dollars that have suddenly become very expensive, but following all the IMF has its headquarters in Washington.

Those who have not lived through this crisis cannot imagine the trauma it represented for Asia.

And suddenly, this crisis has had profound consequences on the world economy for two decades.

The thesis that I live to defend is therefore the following: the sole purpose of all economic policies in Asia since 1998 has been to never see the IMF once more.

- Which leads to a first question: how to never see the IMF once more, and to that the answer is simple: never once more be a debtor in dollars.

- Which brings me to the second question, which the attentive reader will have anticipated: how to never be a debtor once more, that is to say how to have surplus current accounts all the time?

- The same reader, always as attentive, will answer: by having currencies undervalued perpetually, that is to say by following “mercantilist” policies Because the goal of any mercantilist policy is to accumulate sufficiently large foreign exchange reserves so that you never need to borrow abroad once more.

- The last question is of course: how and where will these excess foreign exchange reserves be invested by the countries that have accumulated them? In the distant past, and perhaps in the near future, in gold. Since 1945, in US treasury bonds, since the dominant energy, oil, must be paid in US dollars.

Let’s summarize.

- Asia imports oil, which it pays in dollars.

- All Asian countries trade with each other by settling balances in US dollars.

- The dollar needs of these countries are therefore gigantic.

- To get those dollars, each Asian country must therefore have trade balances with the USA, the only supplier of dollars, the alternative being to borrow some if necessary, which no one wants to do since the disaster of 1997.

- To be certain of having surpluses, you have to maintain an undervalued exchange rate all the time.

- These perpetual surpluses automatically lead to a considerable increase in foreign exchange reserves for countries that follow these policies.

- But that also means that economic growth in Asia is not optimal since trade between Asian nations is not a function of the marginal profitability of capital in the region but a function of the need to have dollars.

- This also means that in countries outside Asia, consumption growth was stronger and investment weaker.

Which brings us to the subject of this paper: how have these “essential” reserves been invested over the past twenty years, but also how will they be invested in the years to come and what will be the consequences of a change in practice of central banks in their investments if they decide to change.

Let’s start with the past and the frantic search for current account surpluses by all Asian countries.

We can clearly see the shift at the beginning of the century, following the Asian crisis.

These perpetually surplus current accounts lead to an upward explosion of foreign exchange reserves, foreign exchange reserves being only the historical sum of current accounts (to put it simply).

CQFD.

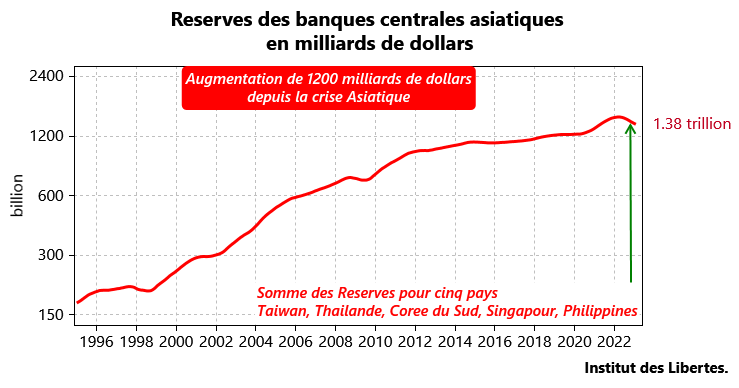

The mercantilist policy followed by all Asian countries has therefore led to an increase in foreign exchange reserves of approximately 1,200 billion dollars since 1997, which is gigantic.

Let us remember here that having abundant reserves in the American currency was vital for these countries since they all needed dollars first to buy oil, and then to trade with each other. There is therefore no question of taking the slightest risk with this war chest. Around 70% of these reserves therefore had to be invested in US bonds and the rest in euros.

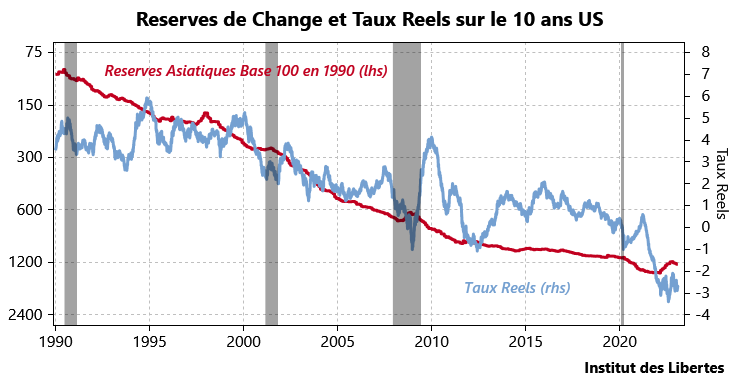

Let’s go back to our bathtub problem and inflows and outflows.

Normally, the interest rate is what balances the supply and demand for savings in a country. Everyone will understand that if, all of a sudden, Asia starts saving like crazy and places these savings in dollars, the supply of savings will increase on the US interest rate market while demand will remain the same. .

This means that the price of savings, that is to say the interest rate in the USA, had to fall in the USA but also in Europe.

And in fact, from 2000 to 2020, we had a deep decline in real interest rates in Europe and the USA.

And this movement was accentuated of course by the follies of the European or American central banks during the last decade, buying government bonds as if there were not going to be enough for everyone (which happens enough rarely).

So we had in our countries an uninterrupted fall in real interest rates for almost twenty years under the triple effect of central banks throwing their caps over the mills, undervalued Asian currencies, preventing any rise in prices here and an oil price under control due to fracking oil in the USA.

And in Asia the reverse.

But, as far as Asia is concerned, things are changing.

- It appears more and more that the dollar will lose its monopoly on oil transactions. Everyone will be able to buy the oil they need using their national currency.

- As I have been writing for a few years, a new monetary system is emerging in Asia and this system will ignore the dollar, which means that Asian countries will no longer have need dollars to trade with each other..

- For the rich people of Asia or the Middle East, it appears more and more that the legal certainty of our countries is not worth tripette and that their rights of property are far from being guaranteed if they invest in Europe or in the USA .

In clear terms, dollar imperialism is overand continuing to accumulate foreign exchange reserves, “in case” THE IMF comes back, is no longer of any use, firstly because these reserves are already gigantic and then because the dollar is no longer of much use.

This means that the Asian currencies will rise since the drain has been closed, and that the dollar and the euro will fall once morest them. But this means that interest rates in the USA and Europe will go up since the tap is closed while they will go down in Asia.

Consequence: Consumption will rise in Asia and fall in Europe and the USA. We will have to work more to earn less in Europe and the USA, while in Asia it will be the opposite, which makes the debate on pensions somewhat surreal.

Which also amounts to saying once once more that you should not have bond investments either in Europe or the USA, but only in Asia, and perhaps in Latin America. Incidentally, sell your real estate in Paris (if you find a buyer) and buy in Singapore or Seoul…. I will return there in the coming months, without a doubt.