TRIBUNE | What an incongruous question! Isn’t it obvious that, driving up rents and capital values, inflation is an unwavering ally of real estate?

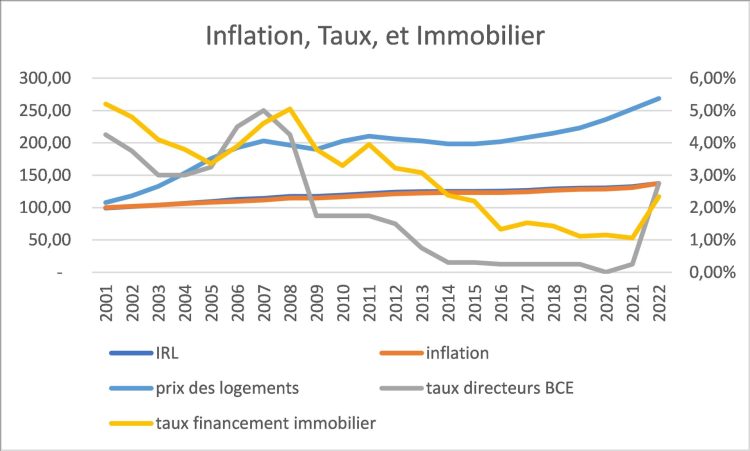

Over the first twenty years of the century, of course, its support was not necessary: while French inflation experienced a historically low rise of 28.75%, the value of real estate rose by 175% (and much more in Paris). The influx of capital and the scarcity of assets – aggravated by sometimes insufficient public policies – have done the job.

Then, from 1is January 2021 to December 31, 2022, inflation jumped to just over 10%. All in good time ! the donors might have exclaimed. L’IRL follows the general inflation rate calculated by INSEE to the millimeter. Even if the law of August 16, 2022 capped the annual rent adjustment at 3.5% until June 30, 2023, the growth in rental yields is significant.

But that’s not all: the first determinant of the capital value of real estate is the rental yield. Therefore, if the latter increases, the price of assets increases mechanically. This gives investors a short-term profit and another in the longer term.

As if that were not enough, credit accounts for 18% of households’ gross real estate assets (8,160 billion euros at the end of 2019). However, the cost of financing excluding insurance remained below 2% from 2016 to 2021. And in France, we borrow at a fixed rate. Therefore, in the event of a rise in rents, the net income of the investor continues to increase – without risk of reversion since rents are not adjustable downwards in the event of disinflation. Incidentally, in the event of an increase in inflation, the debt burden is negative in constant euros. Inexhaustible charms of leverage…

As in everything, however, excess is dangerous. And it is in several ways.

On the one hand, the right of landlords to increase rents sooner or later comes up once morest an elementary limit: the solvency of tenants. If the latter can no longer afford to pay a higher rent, they leave for a smaller, more distant dwelling. Or default on their rent. In the absence of a significant increase in wages and therefore in average purchasing power, which lessee will agree to replace them for a higher rent?

This risk seems all the more acute since, when there is an annual rent review, it has already been 12 months since the tenant was hit in the wallet by food and energy inflation. Its purchasing power is already well eroded, and donors bear the brunt of this “delay effect” : the higher inflation has been over the past year, the greater the risk that they will see downward pressure on rents.

On the other hand, we must never forget that investing in real estate means building, renovating, rehabilitating. Comply without delay with heavy obligations to bring energy strainers up to standard. However, the cost indices for construction or renovation work show an average increase of 15% over the last two years. Budget planning becomes a high-flying exercise.

Having considered all of this, we didn’t mention the elephant in the corridor: rising rates. Central banks have indeed drawn the decisive weapon in their almost sacred fight once morest inflation. Suspicious, credit institutions raise their margins. Buyers and investors are financing themselves today at 2.59% (excluding insurance) while they were financing themselves at 1.06% in 2021. This does not seem like much. However, on a 20-year loan, the impact is considerable: the cost of a loan in fine goes from 21.2% to 51.8% of the acquisition price of a property. Self-financing over 20 years of an asset yielding more than 6% rental yield, it’s over!

And the rate hike, explosive but still far behind inflation, is far from over.

So, thank you inflation?

Let’s do a retrospective exercise: if we had been told in January 2020 that we would have a galloping rise in prices caused in particular by a global pandemic and a war in Europe, and that interest rates would increase in an accelerated fashion, what would have we bet for real estate? A crash, for sure.

S’is it produced? Or are we at the heart of whatAlan Greenspan called a conundrum[1] ?

Maybe. Or not. The almost uncontrollable drift of inflation is a squall that shakes the two pillars of the real estate market: the rental yield and the attractiveness of the investment. The supporting factors of demographics and economic growth are there to ensure long-term growth. But in the short term, the signals have turned orange: lower transaction and credit volumes, lengthening of sale deadlines, systematic price negotiations by buyers. The market is far from collapsing, of course. But the downside pressure is there, visible, and starting to make a lot of noise. Which, in German, is called “crash”.

Tribune signed by David Aubin, president of AtlantiStar

[1] problem to which no clear answer can be given.

<<< A lire également : Inflation, choc économique, conformité : le DAF contre Goliath ? >>>