Russia’s debt default in August 1998 triggered the financial crisis. At that time, the US hedge fund LTCM was on the verge of collapse, and the Federal Reserve (Fed) urgently asked Wall Street banks to bail out. Now this threat is approaching once more, and Russia is worth more than 100 million yuan.DollarBonds will mature this Wednesday (March 16), and everyone is concerned regarding whether it will hit global markets once more.

Russia will have 117 million this WednesdayDollarofDollarAs denominated bonds mature, Russia’s finance ministry said on Monday it was ready to pay, but might not get itDollar, will be paid in rubles.Analysts pointed out that if it cannot be used within the 30-day grace period,DollarPaying interest is like repaying debt. Fitch, the credit-rating agency, slashed Russia’s credit rating last week to just one notch above default.

But Capital Economics emerging markets economist William Jackson said the default was symbolic and at this point looked unlikely to have a significant impact on Russia and other countries, although there were two risks to be aware of.

Jackson said the biggest cost for Russia would be isolation from global capital markets, or at least high borrowing costs for an extended period of time, but the string of sanctions so far has dealt the same blow .

The head of the International Monetary Fund (IMF), Kristalina Georgieva, also said that although Russia has the money to repay its debts, the series of sanctions imposed on financial institutions and the central bank means that Russia cannot use the funds, and a Russian default is no longer “impossible” to happen. event.But the IMF does not think it will cause a global financial crisis, on the grounds that although the banking industry has an exposure of regarding 120 billion in RussiaDollarbut not systematically related.

For foreign investors, the risk of a Russian default has largely been priced in.RussiaDollarThe price of denominated sovereign bonds has plummeted and is now worth just 20 cents.

Many media also reported that creditors have already significantly reduced their holdings.Russia’s foreign currency sovereign debt held by non-resident Russians is “relatively small” at around $20 billion, Capital Economics’ Jackson said.Dollar。

Two potential risks: unknown exposure of institutions, default of Russian companies

However, Jackson noted that there are still two risks to Russia’s insolvency worth noting. First, under the overall numbers,There may still be an institution with a systemically important risk holding substantial amounts of Russian sovereign debtwhich may bring regarding a butterfly effect in global financial markets.

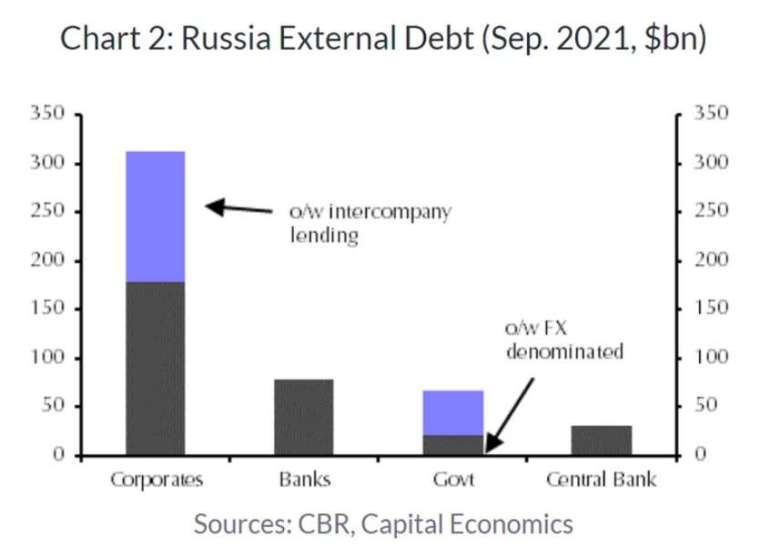

Second, Russia’s sovereign debt default may be a prelude to a Russian corporate default, andRussian corporate external debt far exceeds sovereign debt。

Jackson said that while countries continue to tighten sanctions, Russian companies can continue to pay their debts for now, but if transactions are disrupted, sanctions expand and the economy sinks into a severe recession, the possibility of Russian companies defaulting will increase.